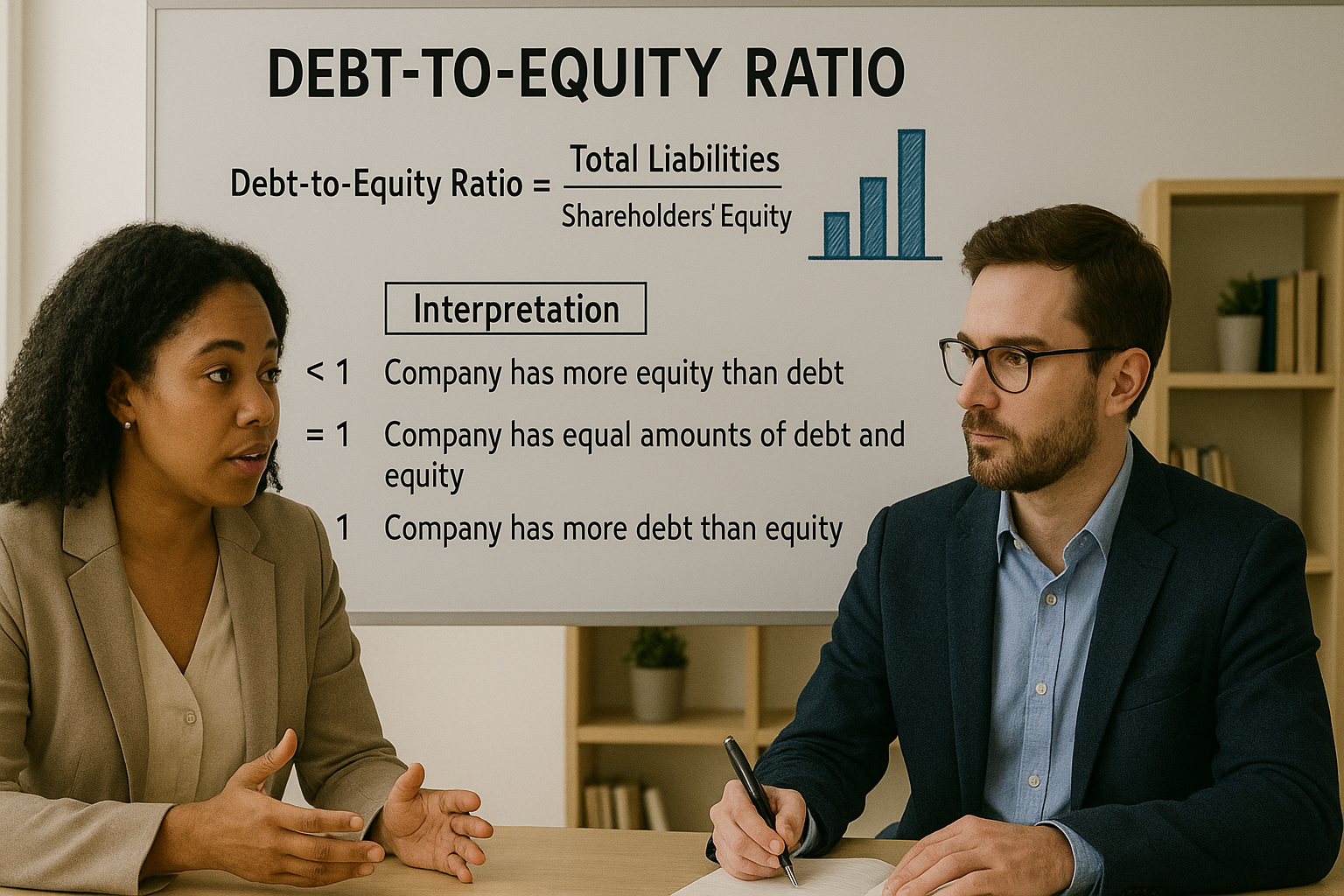

Leverage indicator

Measures the extent to which a company is funding its growth with debt versus equity.

The D/E ratio directly ties into the balance sheet. It influences:

Risk assessments by lenders and credit rating agencies.

Cost of capital — higher debt increases interest expenses.

Return on equity — leverage can amplify returns when used effectively.

Case study:

Tata Motors’ evolving debt-to-equity strategy

In the early 2010s, Tata Motors took on significant debt to fund the acquisition of Jaguar Land Rover. This pushed its D/E ratio above 2.5, raising investor concerns. Over the next decade, the company focused on deleveraging through improved cash flow and asset sales. By FY24, Tata Motors had brought its D/E ratio closer to 1.5 — signaling improved balance sheet health.

This evolution showcases how strategic debt management can balance growth and financial discipline.