5 minutes read

Living in India and earning in another currency? You have probably realized the value of keeping your earnings in foreign currency to pay for your overseas expenses. Instead of paying for FX conversion twice, one can open an EEFC (Exchange Earners’ Foreign Currency) account with an Indian bank.

The Reserve Bank of India made amendments to the Foreign Exchange Management Act, 1999, allowing “opening, holding, and maintaining” Foreign Currency Accounts in India in May 2000. The regulations came into force a month later.

What is an EEFC account?

An EEFC account is an account maintained in foreign currency in India. Those based in India, but earn in foreign currency can open an EEFC account. Only an authorised dealer can open and maintain an EEFC account for you. An authorised dealer is a bank authorised to deal in foreign exchange. The authorised dealer can be private or state-run.

You can save on fees, and get much better exchange rates than an EEFC, with a Winvesta Multi-Currency Account.

Winvesta Multi-Currency Account allows you to save and transact in 30+ currencies with your own account details including IBAN, sort code, and more. Get started in minutes, whether you are an individual or a business.

Are there any restrictions with an EEFC account?

An EEFC account allows you to credit 100% of your foreign currency earnings. It is, however, subject to a condition. On or before the last day of next month, the total accrual during the month will have to be converted into rupees. You can still retain foreign currency in the EEFC account for approved purposes or prior commitments.

For Example: If an individual has deposited $100 in his EEFC account during the month of May, he must, by the end of June, convert the balance amount then into Indian rupees. However, if he must make a payment of say $40 in July, he can retain that amount in the EEFC account and convert the balance amount of $60 to INR.

Who can open an EEFC account?

- Any individual professional can open an EEFC account. Professions include any freelancer, doctor, lawyer, artists, architect, engineer, consultant, chartered accountant, director on boards of overseas companies, or others.

- Among corporates, a 100% Export Oriented Unit (EOU), or a unit situated in an Export Processing Zone (EPZ), Software Technology Park (STP), or an Electronic Hardware Technology Park can open such an account. Such units can now credit 100% of their foreign exchange receipts into such accounts, from the earlier 70%.

Is there any interest on the cash in EEFC accounts?

You can operate an EEFC account only as a current account. No interest is payable on such accounts.

How to Open an EEFC Account?

As mentioned earlier, only the banks that deal with the foreign exchange can open EEFC accounts. Major Indian banks like ICICI, HDFC, Axis, IndusInd, and DBS, offer EEFC accounts.

Documents Needed To Open An EEFC Account:

- A completely filled-in and signed EEFC account opening form.

- Documents like board resolution, partnership letter, proprietorship letter, which authorise the opening of such an account. Specify the currency in which the account is to be opened in any of the documents you submit.

- Proof of Status – Whether the unit is located in an SEZ, STP or ETHP.

- Nomination form – If the customer has given consent for the same. These forms are only applicable to individuals and sole proprietors.

- Proof of PAN / Form 60

- NOC from the lending bank(s) extending credit facility to the entity, if applicable.

- Individuals opening such an account will require identity and address proof of all authorized signatories.

- Partnership firms will require a partnership deed duly stamped and signed by all partners along with identity proofs of all authorised signatories.

- A Hindu Undivided Family (HUF) looking to open such an account will require a letter signed by Karta and all major coparceners. Photograph and specimen signatures of Karta and Coparceners will also be needed along with the identity proof and address proof of the Karta. One cannot include a female member as a Coparcener.

One of the benefits of an EEFC account is that it avoids double-conversion costs for the customer. On payment in foreign currency, an account holder can hold the sum in the same currency without having to convert it into rupees. The conversion charges that banks levy can however be quite high. See below for how to avoid those.

For example: As an exporter, if you have to receive a payment of $10K, a normal current account will require you to convert the payment into rupees, for which your bank will charge a certain transaction charge. A few days later, if you need to make a payment for imports, you will again have to pay transaction charges to your bank for converting your rupees into foreign currency. An EEFC account can avoid these requirements.

Special Economic Zones

Special Economic Zones (SEZ) cannot open EEFC accounts.

However, a unit located inside an SEZ can open such an account with an authorised dealer outside the SEZ, subject to these conditions:

- This account will credit all foreign exchange funds received by the unit.

- An EEFC account cannot credit any foreign exchange purchased in India, against rupees, without prior permission from the RBI.

- Provided these funds held in such accounts will not be lent or made available in any manner to any person or entity resident in India, that is not a unit in an SEZ.

- The funds in the account shall be used for bonafide trade transactions of the unit in the SEZ with a resident of India or otherwise.

Permissible Credits Under EEFC Accounts

- An EEFC account can credit any inward remittance. However, it needs to be noted that remittance in the form of a foreign currency loan or foreign investment CANNOT be credited to such accounts.

- Professional fees including directors’ fee, consultancy fee, lecture fee, or for any other professional service carried out in individual capacity.

- Payment in foreign currency by a firm in the domestic tariff area for the supply of goods to a company situated in an SEZ.

- Advance remittance towards export of goods or services.

- Re-credit of unutilized foreign currency earlier withdrawn from the account.

- Proceeds received by the account holder on the conversion of shares into ADRs or GDRS under the sponsored ADR/GDR scheme of the Government of India can also be deposited into such accounts.

Permissible Debits Under EEFC Accounts

- Outward payments towards permissible current account transactions.

- Any payments in foreign currency towards the purchase of goods from a 100% Export Oriented Unit or a unit in Export Processing Zone or Software Technology Park or Electronic Hardware Technology Park.

- Payment of customs duty in line with the Foreign Trade Policy.

- Payments to a person who resides in India for the supply of goods and services, including payments for airfare and hotel expenditure.

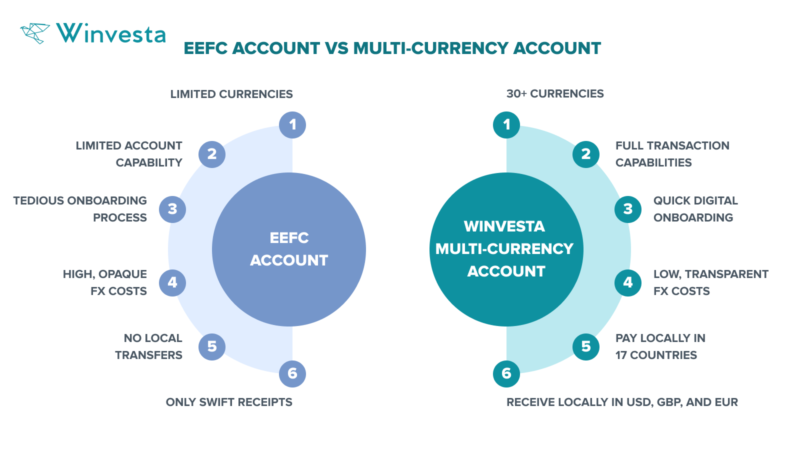

The Problems With An EEFC Account:

There are two main problems that individuals and businesses face with an EEFC account:

- Account opening process: It is extremely document-intensive and time-consuming to open an EEFC account with a bank. Banks can take several weeks to approve and activate an account.

- FX conversion charges: The fixed fee and spread for converting foreign currency into INR is often not transparent and can be quite high.

Can Indian residents and businesses open a foreign currency account outside India?

Yes. Individuals (including freelancers) can open and maintain foreign currency accounts overseas. There is no requirement to remit all the foreign earnings back to India, unlike the EEFC account. Indian businesses can also maintain a foreign currency account overseas.

Winvesta Multi-Currency Account – the smarter alternative to EEFC accounts

Winvesta offers secure multi-currency accounts in the UK for individuals and businesses. These e-money accounts are held with an FCA-regulated e-money institution. Your cash is safeguarded with Tier 1 banks like Barclays in the UK. Here are some advantages of the Winvesta Multi-currency account against the EEFC:

- 30+ Currencies: Winvesta MCA offers individual accounts in 30+ currencies, including USD, GBP, and EUR. All on one platform. You can convert and transfer money between accounts free of cost.

- Your own foreign accounts: The accounts are in your name, and come with details like sort code, IBAN, routing number, and more.

- Quick digital onboarding: It takes only minutes to sign up for an account. Most individual accounts are approved and activated the same day. It takes approximately two business days to approve business accounts.

- Low, transparent FX costs: Convert between currencies without any fixed fee. See the FX rate before conversion.

- Local payments to 17 countries including India: Save money on international wire transfers by using our local remittance capabilities. You can convert funds to INR within the account at a transparent FX rate, and then make a domestic transfer to your Indian bank account.

- Local receipts: Receive money locally in USD, GBP, and EUR. This means an easy collection for you, and less hassle for the sender.